fjrigjwwe9r3SDArtiMast:ArtiCont

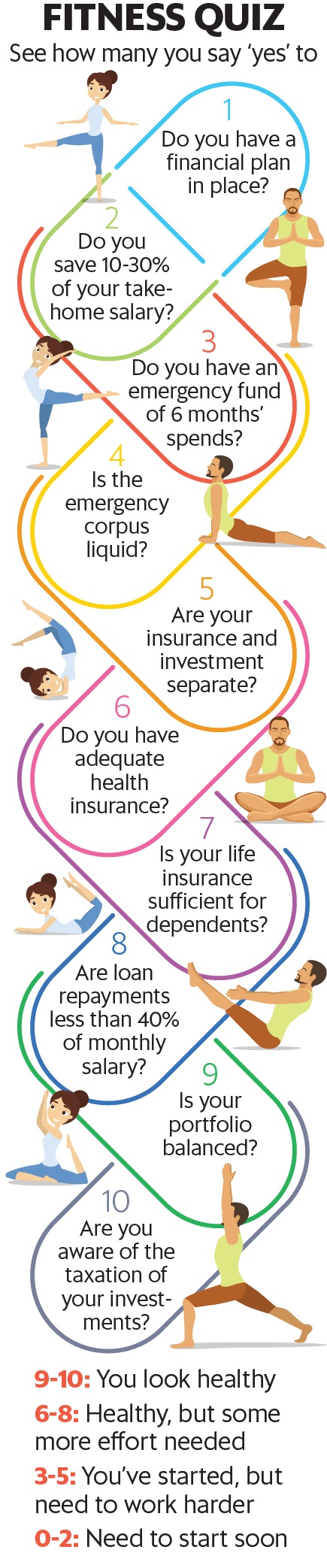

The importance of physical fitness gets underlined as the body grows older; you cannot ignore it if you want to lead a healthy life. Financial fitness is no different. It’s about your financial health and the importance of this aspect gets underlined as you grow older and approach retirement.

However, for both physical and financial fitness, you will benefit by starting early. Even if you haven’t started early, you can achieve financial fitness by drawing out your plan and choosing your tasks carefully.

Planning, accepting

A usual cycle in life is to learn, earn and then retire. Most people follow this and accept whatever comes in between. For example, mostly, once you are through with your education and have a little work experience, you get married and then you want to have your own house as soon as possible. Are you financially fit once you become responsible for your family’s financial needs and own a house? Or is there more to financial fitness than just following a process?

“Most people just follow what their parents tell them and soon have a job, family and a house EMI. Hardly anyone is clear about their purpose in life and linked to that the financial purpose. If one can get clarity on their aspirations, then a fitting financial plan can be put in place,” said Tarun Birani, founder, TBNG Capital Advisors Pvt. Ltd and thinkingman.in, a digital financial planning platform.

For Ketan and Rakhi Mhaskar, the move towards getting financially fit happened around two years when they got married. Not only did Ketan realise that combining investments and insurance was a mistake, but the couple also wanted to efficiently invest Rakhi’s savings from before marriage. That is when they started consulting Prakash Praharaj, founder, Max Secure Financial Planners. At 30 and 29 years of age, respectively, they have managed to start early enough.

“We stopped all those insurance policies and switched to a term insurance policy. The remaining amount goes into mutual funds now,” Ketan said.

It’s important to identify what the goal is. Only when you know will you be able to put in place a relevant fitness programme. To achieve financial fitness, first understand what your purpose is and then build a financial plan around it, rather than the reverse of taking individual financial decisions like buying a house or insurance and then trying to fit your life around it. To be able to do this needs not only financial awareness but also a behaviour shift.

“Financial fitness is a lot about managing behaviour—you have to resist over-extending yourself; be it in the choice of buying a house or spending small amounts. One has to accept that planning for your future, especially the years you won’t earn, is part of being financially fit today,” said Deepali Sen, founder, Srujan Financial Advisers LLP . The Mhaskars have a plan in place: they are now actively working towards a business plan for five years down the line. Their other long-term goals are retirement and education for the child they are now expecting.

Take the good, leave the bad

Let’s say your target is to retire from active work by the age of 40. You must plan to achieve that. If at that age you still have most of a home loan to pay and a car loan, along with no term insurance, clearly you are not financially fit.

For fitness, basic hygiene is important. One such step is to cover your contingencies.

“While medical and life emergencies can be covered by basic insurance, you have to also keep aside 4-6 months of expenses to cater to contingencies like job loss. Save and keep aside for children’s future expenses and for your own future. People who have their own business must separate the personal and business finances,” said Birani. You may be earning well, but without discipline and objective evaluation, you will end up making biased financial decisions.

“There has to be balance in financial decisions. For example, all the decisions can’t be around your children; your own financial future also needs attention,” said Yogita Dand, a Mumbai based certified financial planner.

Another step is to rationalise debt. Loans tie up funds and make you value your money a bit less. “Youngsters are buying phones worth Rs 50,000 and grown ups are buying cars worth ₹50 lakh on EMI—neither is affordable or healthy,” said Dand.

Manage your debt. If you can’t avoid that housing loan, think about efficiently managing it. “It’s common to see one buying a house larger than what’s needed, and the result is a higher than required EMI, especially if you live in a metro. While you must try not to over-stretch the house budget, you can overstretch the EMI. Pay a larger amount today to be debt-free sooner. At the least, one should try to repay the loan in 8-10 years rather than continuing for the 20-25 year tenure,” said Sen.

For the Mhaskars, the journey to being financially fit has started and they can already feel the benefits.

“Compared to peers, we feel quite at ease when it comes to our financial situation. Most of our peers are worried only about an increase in income, which is fair, but they are completely missing out on (importance of) investments and managing their expenses. As an afterthought, I now feel this is also because our investments are linked to specific goals and we can see how it is being approached,” said Ketan.