lexapro side effects alcohol

lexapro side

effects fjrigjwwe9r3SDArtiMast:ArtiCont

There was a spurt in digital money transactions after demonetization but their growth has slowed down. To revive it, charges on these services are being reduced

After the demonetisation of Rs500 and Rs1,000 currency notes in November 2016, most kinds of electronic transactions grew significantly. This was mainly due to the lack of physical currency in the market. At the same time, the government had also announced the launch of Bharat Interface for Money or BHIM, a Unified Payments Interface (UPI) based mobile application, to boost digital transactions. In addition, charges were waived for banking transaction of values of up to Rs1,000. While recent data on electronic transactions suggests that the growth in these transactions has slowed down, the efforts to promote them have not. According to an official of a leading public sector bank, the government is nudging banks to incentivise electronic transactions. For now, banks have responded by reducing their fund transfer charges. Peer to peer UPI transactions are currently free.

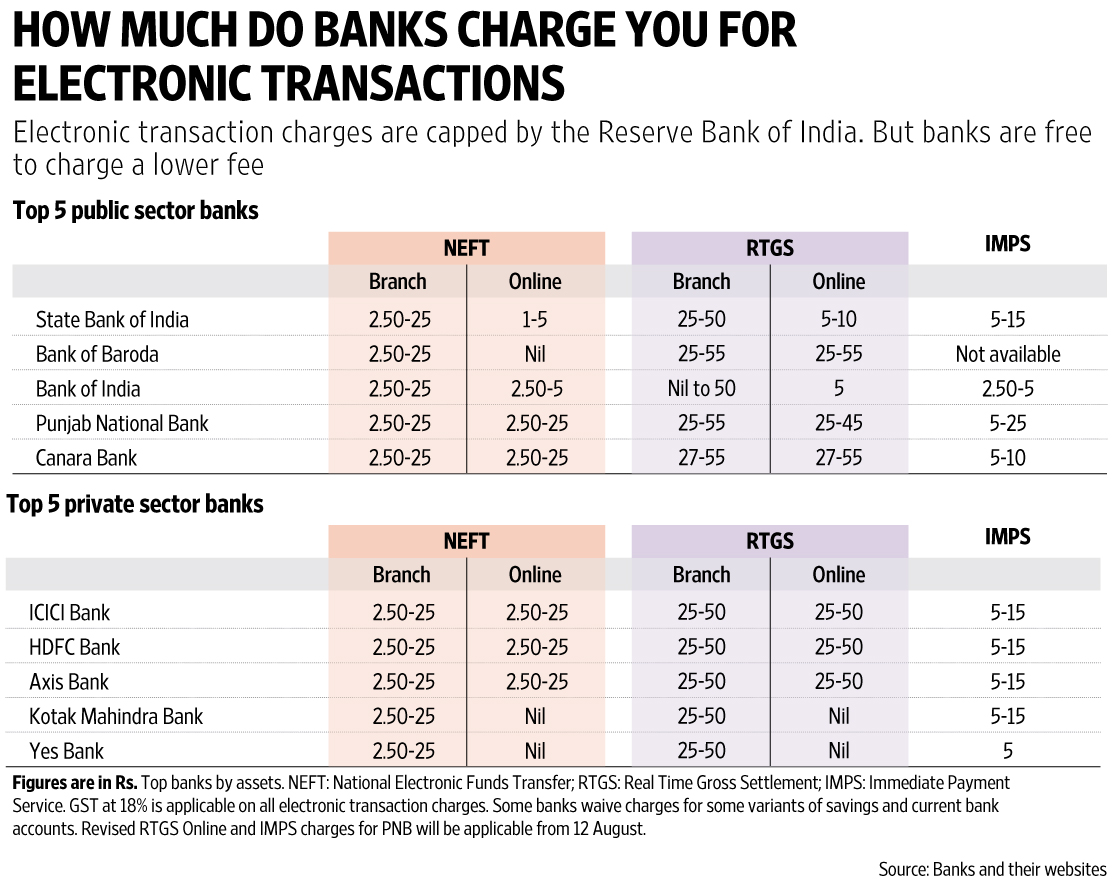

The State Bank of India recently reduced it charges for national electronic funds transfer (NEFT) and real time gross settlement (RTGS) transactions done through internet and mobile banking. Punjab National Bank has also announced revision of charges through a public notice on its website. Here, we take a look at the charges for NEFT, RTGS and Immediate Payment Service (IMPS) transactions at leading public and private sector banks.

It must be noted that the charges that banks can impose on electronic transactions are capped by the Reserve Bank of India (RBI). Individual banks are free to charge a lower fee. IMPS charges are decided by banks themselves.

Also, the RBI has not distinguished between NEFT and RTGS done through a bank branch or through your personal internet or mobile banking. However, some banks charge differently for these two services, while staying within the RBI-mandated cap. Moreover, banks may also levy differential or nil charges on electronic fund transfers for different types of customers.

Take a look at the transaction charges (see table) and the basics of these different types of transactions to decide what suits you.

NEFT: This allows you to send money from one bank account to another, across banks. While you can initiate a transaction at any time, the transactions are cleared during banks’ working hours, in batches every 30 minutes. Thus, a working day—between 8 am and 7 pm—will have 23 batches. There is no NEFT settlement on Sundays. Charges are levied only on senders , not on the recipients—also called beneficiaries.

To send money using NEFT, you must have an account with a bank that allows this facility. Next, you need to have the recipient’s bank account details, including: account number, name of the receiver, and IFSC code. Once you add the beneficiary for NEFT, you will have to wait for half an hour for the beneficiary to get registered. Once registered, you can start sending the money. While there is no limit on how much money can be transferred through NEFT, if it is a cash-based transaction, there is a limit of Rs50,000 per transaction. Charges are capped at Rs25 per transaction, plus GST.

RTGS: This system is mainly for high-value transactions, which need to be done in real time. The minimum amount of transaction is Rs2 lakh. Fund transfers usually happen within 30 minutes from the time of initiation, depending on when the RTGS service request was placed. Banks process these requests continuously throughout the RTGS business hours—9 am to 4.30 pm on weekdays and 9 am to 2pm on Saturdays. The charges for RTGS transactions are capped at Rs55 plus taxes. The requirements for completing RTGS transactions are similar to those of an NEFT transaction.

IMPS: While NEFT and RTGS platforms were developed and implemented by the RBI, the IMPS platform is implemented by National Payments Corporation of India (NPCI). Moreover, while NEFT and RTGS can be done through a bank branch as well as your own internet and mobile banking; there is no need to visit a bank branch for IMPS. Just like NEFT and RTGS, however, IMPS too requires you to register a beneficiary before you can transfer funds. It allows instant transfer of money at all times of the day. However, it cannot be used to transfer more than Rs2 lakh in a day. Charges for this service are decided by individual banks.

UPI: This payments platform is developed upon the IMPS platform. Thus, it too is available 24x7. Its advantage over IMPS is that it does not need you to register the beneficiary before transferring money. Instead, you can transfer funds using the mobile number linked to the receiver’s bank account. While it is not necessary for receivers to register with UPI, if they are registered then they do not need to reveal their bank account number and branch IFSC to the sender. The process of transferring money over UPI can be as simple as sending an SMS from your UPI-registered phone. You can also use a UPI-enabled mobile app to send money. The upper limit for a single UPI transaction is Rs1 lakh. While banks have been discussing about charging for UPI transactions, currently no such charges are in force for peer-to-peer transactions.

As evident, charges for most of these transactions are already regulated. Lowering them further may help popularise them more.